Index

- Introduction

- A Green And Inclusive Way Of Thinking

- Components Of Integral Thinking

- Green Thresholds – Planetary Boundaries And Doughnut Economics For A Green And Sustainable Earth

- A Systems-Based Approach For A Green And Inclusive Economy

- Contrasting Integral Thinking With Integrated Reporting

- The IIRC’s Framework

- Green And Inclusive Reporting

- The Benefits Of Green And Inclusive Reporting

- Moving Forward

- Why Is it Essential That We Focus On Integral Thinking?

- Achieving The United Nations Sustainability Development Goals (SDGs)

Introduction

Integral Thinking has developed in recent years, promoting the focus on a green and inclusive economy (Thurm, 2016). It underpins the ways all actors should consider performance with respect to social and environmental, along with economic areas. Yet, in some ways, Integrated Thinking and Reporting has co-opted this approach as a focus.

Source: Freepik

A Green and Inclusive Way of Thinking

Integrated Reporting has taken off recently. Unlike Integrated Reporting, Integral Thinking is a theoretical framework that is holistic and interconnected. This holistic approach measures the social, economic, and environmental impacts of any group, product, or service (Steger et al., 2018). An integral perspective exists in this holistic approach (Wigboldus et al., 2021). In fact, this allows holistic and interconnected measurements of all activity to ascertain sustainability (Thurm, 2016). In other words, it is not just focused on what a company can disclose, as with Integrated Reporting.

Integral Thinking demonstrates the need for multiple perspectives to measure sustainability (Steger, 2018). Integrated Thinking and Reporting, on the other hand, is largely what companies have used in recent years. Companies use Integrated Thinking and Reporting to demonstrate levels of environmental and social impacts in an integrated way. But this has not necessarily used key components of Integral Thinking. Integral Thinking, as the backdrop behind this, goes much deeper.

Components of Integral Thinking

There are many theoretical approaches that guide Integral thinking. For instance, to supply optimal parameters, metrics, and strategies in thinking and to enable effective integral measurement of sustainability. These, for example, include Materiality, Context-Based Metrics, and a Multi-Capital approach (Thurm, 2019). All these approaches help to inform the framework of Integral Thinking.

Global Thresholds – Planetary Boundaries and Doughnut Economics for a green and sustainable earth

A big part of Integral Thinking is the utilisation of global thresholds. These global thresholds guide the framework of measuring sustainability (Thurm, 2019). Two such Global Threshold approaches are Planetary Boundaries (Steffen et al., 2015) and Doughnut Economics (Raworth, 2012).

Planetary Boundaries demonstrate a clear template of affected planetary areas such as climate change or ocean acidification. These boundaries or thresholds guide the evaluation of the effects of products or services (Thurm, 2019). These informing planetary boundaries safeguard different areas, such as climate change, freshwater use, and biodiversity loss (Steffen, 2015). Planetary boundaries, as a reflection of global thresholds, are essential to Integral Thinking. Furthermore, they create underlying key parameters that industries must operate within to preserve environmental interests and the planet’s biosphere. Planetary Boundaries are a tangible template for determining the boundaries of biosphere integrity. Therefore, Planetary Boundaries are of significant relevance and use for Integral Thinking as guiding parameters (Thurm, 2019).

Doughnut Economics, similarly, acts in a way to prevent environmental impacts through an economic lens. It acts as a template to demonstrate the optimum position of activity for companies or governments. It helps them avoid encroaching upon environmental concerns while avoiding falling short of addressing social and economic issues (Raworth, 2012). This provides a safe zone in which neither environmental nor social harm exists while operating within these parameters (Thurm, 2019).

A Systems-Based Approach for a green and inclusive economy

Integral thinking also utilises a systems-based approach in recognising the interconnectedness of systems. For example, how green and social systems link to different areas of sustainable business models and sustainability broadly (Steger et al., 2018). A systems approach exists as a framework to measure the sustainability of any product or service. Understanding the interconnectedness of systems is vital to a systems approach. Looking at systems linked to Ecological Theory demonstrates how interconnected systems are both green and societal. They don’t just exist in isolation. Thus, the Integral Thinking approach should focus on mitigating impacts locally and globally (Wahl, 2006), simultaneously addressing different systems of different scale levels. There are four scales in this systems approach. These include: Macro (Economic, Ecological and Social), Meso (Industry, Portfolio, Habitat), Micro (workplace) and Nano (Individual) (Thurm, 2019). Each of these should intersect with measuring sustainability but in a holistic, green and interconnected way.

However, if a company reports on its sustainability performance using Integrated Reporting, it is not necessarily adopting a systems approach broadly; they can still have an insular focus on social, environmental/green and economic impacts. Rather, companies need the integration of its impact on each level broadly or holistically. This highlights a detraction of Integrated Reporting and Thinking from Integral Thinking.

Contrasting Integral Thinking with Integrated Reporting

Companies have adopted Integrated Reporting as a phenomenon in recent years, originally proposed in alignment with integral thinking. This allows for the disclosure and reporting of environmental and social impacts associated with the running of a company, as opposed to just the financial profits. It’s a contrast to having separate environmental/green and social impact reports. These reports, especially when not linked to financial performance, make it harder to enable a comprehensive assessment of a company’s performance. The idea is that integrated reporting should prevent a fundamental issue that hinders sustainability. It should prevent aspects of a company’s performance from being conceived and reported separately to one another.

In recent years, there has been a bigger drawback to the application and adoption of integrated reporting. This drawback is the lack of emphasis on Integral Thinking as a primary component of what should underpin Integrated Reporting. With the trend of Integrated Reporting having taken off, many companies disclose performance in an integrated way. Integrated Reporting is voluntary. Because of this, some companies will pay lip-service to the IFRS’s key principles and parameters whilst neglecting Integral Thinking to inform company operations and guide the reporting process.

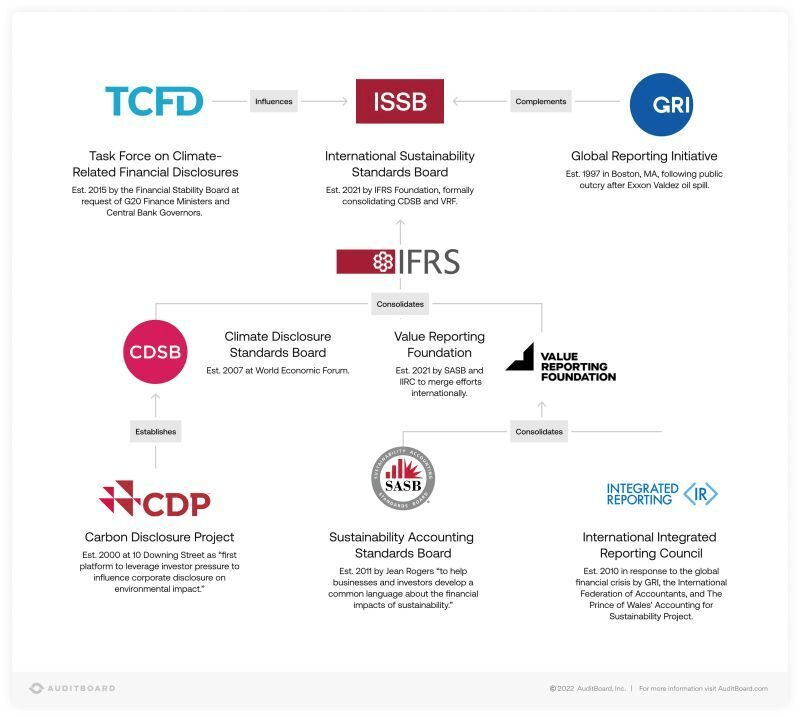

The diagram below demonstrates the progression and influences of different bodies in adopting Integral Thinking and Integrated Reporting and how different influences, such as from the Global Reporting Initiative, and International Integrated Reporting Council came to form the IFRS and the International Sustainability Standards Board in 2021.

Source: ESG Professionals Network.

The IIRC’s framework

According to the IIRC, Integrated Reporting is a framework and model for Integrated Thinking. Integrated Reporting can assist with allocating capital for the betterment of sustainable development and financial stability (IFRS, 2023). Integrated Reporting enables a more cohesive and efficient structure of reporting. This structure covers a full range of factors that materially impact creating value over time. Therefore, it allows for a stronger ability for accountability and stewardship regarding different forms of capital. This includes financial, manufacturing, social, human, intellectual, and natural capital. It also supports integrated thinking, decision making, and actions that create value over time.

In the past, companies have reported upon different issues, in separation from one another, referred to as reporting ‘within Silos’. This causes a lack of consistent standards of reporting across different issues concerning performance. Integrated Reporting, on the other hand, enables a more universalised language and framework. These facilitate easier appraisal of voluntary reporting from a standard viewpoint (Delloit, 2016).

This may be the case for many companies in purportedly supporting Integrated Thinking. However, for many others, Integrated Reporting focuses and emphasises using the IIRC’s framework purely to better economic value over time. Within such parameters, little emphasis is placed on the underlying theme of Integral Thinking, which should be the guiding core of Integrated Reporting.

Green and Inclusive Reporting

IFRS Foundation

The Integrated Reporting Framework merges financial statements and sustainability-related financial disclosures. It exists alongside Integrated Thinking Principles, which are both under the auspices of the IFRS organisation. The IFRS organisation was created to develop high-quality, understandable, enforceable, globally accepted accounting and sustainability disclosure standards (IFRS, 2023). Company attitudes that Integral Thinking only exists alongside Integrated Reporting reveals an insufficient emphasis on these standards. Many companies claim this is an authoritative standard of a universalised framework. It supposedly enables more effective reporting on value creation in terms of financial capital and sustainability across a range of contexts, including green and social (IFRS, 2023). However, by giving more emphasis in authoritative terms to Integral Thinking as a guiding parameter for reporting, this framework could achieve greater authority and success in addressing environmental and social sustainability (Thurm, 2019).

Study

A 2017 study by investors looked at financial reports within two contexts. One is Integrated Reporting, and the other is a separate sustainability report with assurance of sustainability information. This study demonstrated that Integrated Reporting had little bearing on the decision-making of investors, due to investors’ predisposition to sustainability as a motivating factor. Assessing the assurance of sustainability, as opposed to non-assurance, had a more significant impact, while Integrated Reporting enabled a higher degree of measuring sustainability performance (Reimsbach et al., 2017). Integrated Reporting doesn’t just verify sustainability claims from assurance of sustainability. It has a greater capacity to measure the degree of sustainability across a variety of different areas.

This, in itself, however, doesn’t bear a greater measurement of sustainability if Integral Thinking isn’t integral to the process. Furthermore, the context-based measurement of a company’s performance, for instance, might demonstrate appalling environmental impacts compared to other companies.

Furthermore, it is possible to create a positive spin based on comparative figures to previous years’ performances.

Source: Freepik.

Benefits of Green and Inclusive Reporting

According to one study, Integrated Reporting also has the capacity to influence internal decision-making. Internal decision-makers tend to appraise the sustainability and direction a firm has and are more motivated to sustainable value creation. Thus, Integrated Reporting can influence companies’ behaviour in making sustainable decisions (Esch et al.,2019). This enables positive influences for both investors and company decision-makers. However, one study in undertaking a systemic review of the literature of Integrated Reporting suggests further investigation is needed. Specifically regarding the concept of ‘value creation’, internal and qualitative determinants, as well as the quality and content of Integrated Reporting (Vitolla et al., 2019).

Despite influencing internal decision-making for companies, Integrated Reporting without Integral Thinking may not mitigate environmental and social impacts in a targeted and real sense. It can enhance effective operations in Integrated Reporting on progress for better value creation whilst neglecting real-world mitigation of environmental/green and social impacts.

According to Feng et al., (2017), Integrated Reporting stakeholders lack a clear consensus and understanding of what Integrated Thinking means. In contrast, Integral Thinking is much clearer. Thus, whilst Integrated Reporting has been a significant focus for companies recently, Integral Thinking has not. There has been a lack of clear understanding, definition, or consensus on how Integral Thinking should guide reporting. This demonstrates a significant issue in how a substantial portion of Integrated Reporting is conducted. A significant rift exists between Integral Thinking and Integrated Reporting.

Many industries adopted Integrated Reporting across the board. We must not overlook Integral Thinking in the application of Integrated Reporting. Integral Thinking must be a larger overall guiding focus of reporting. It’s a central tenet and determinant of a company’s operations and accountability through more standardised reporting systems.

moving forward

Integrated Reporting must be based on Integral thinking as an underlying philosophy. In the pursuit of addressing climate, environmental/green, and social issues alongside economic performance, it is crucial not to forget Integral Thinking in assessing performance. It isn’t just companies that need to be mindful of performance in each area. We must consider a holistic understanding of all areas of performance. An understanding for every actor, including institutions, as a means to standardise its application and adherence to this standard.

Why is it essential that we focus on Integral thinking?

Integral Thinking considers how actions impact the planet and society. Actions from people, organisations, and nations. Not just in terms of measuring performance in economic value but in terms of ecological/green and social impacts. Integral thinking directs our society towards improved living standards and a thriving future.

achieving the United Nations Sustainability Development Goals (SDGs)

The United Nations 17 Sustainable Development Goals (SDGs) are important goals to attain. These range from issues in education and human rights abuses to the betterment of life on land and below water. They promote renewable green technology, biodiversity protection, sustainable agriculture, democracies, strong institutions, human rights protection, and protection of natural areas.

THRIVE Framework

THRIVE Project invests interest in issues fundamental to the well-being of our society. This included improving every element of our global ecosystems to create a Thrivable global ecosystem, planet, and society. THRIVE’s mission is to safeguard human well-being in all domains and the well-being of nature and every living being.

To learn more about how The THRIVE Project is researching, educating and advocating for a future beyond sustainability, visit our website. You can follow our informative blog and podcast series, and learn about our regular live webinars featuring expert guests in the field. Sign up for our newsletter for regular updates.